03/03/2021

Antonio de la Torre, Head of Business Performance Management, Strategy & BPM, CFO at Repsol, is an economist and holds an MBA from the IESE. He has been working at Repsol for over 30 years, both as a commercial supervisor of businesses at Repsol Butane and in cross-company roles such as planning, control, business development, and corporate development (M&A). He was a supervisor in the Insurance department for over five years and in the Risks department for just under two years at Repsol. Now, he is beginning a new challenge following the launch of the company’s strategic transition in business performance management under the CFO Strategy Area.

In this interview, De la Torre spoke about the company’s new Strategic Plan, focused on transforming the energy giant into a net zero carbon emissions company by 2050 and what this transformation will entail for the various business lines and for risk management.

Repsol announced its Strategic Plan for the coming years on November 26. Could you briefly explain the focus and the primary foundations of the Plan?

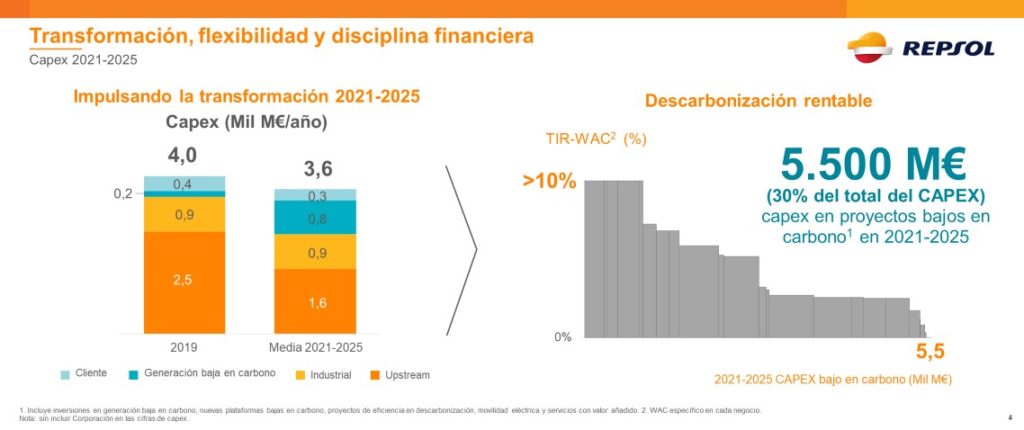

Thank you, MAPFRE, for your welcoming invitation. Repsol’s central objective is to make itself into a net-zero carbon emissions company by 2050 in a cost-effective way while ensuring its growth. This will come with a distinguished ambition of transformation by 2030 alongside greater speed, intensity, and viability in our energy and strategic transition, to which we will allocate more than 30% of our investments in low-carbon projects (€5.5B), in addition to a significant increase in cash flow generation, financial discipline, and attractive remuneration for our shareholders.

To that end, we are going to leverage the two large drivers of cash flow and the solid foundation of assets that will enable us to enact this transition—(i) the upstream business, which covers all the activities associated with exploring, developing, and producing oil and gas and (ii) the downstream business, which includes all the businesses for trading and supply of crude and products, refining and processing crude and products, the chemical business (industrial), the commercial businesses primarily associated with energy and service provision for our extensive service station client base, natural gas, electricity, butane, lubricants, asphalt, and specialties (client), and finally our new growth vector associated with wind, solar, hydraulic, cogeneration, and combined cycle electricity generation (renewable energy generation). In fact, we now have four separate business verticals—upstream, industrial, clients, and renewable energy generation—and the new corporate model that prioritizes responsibility and helps create value.

Repsol’s aspiration is therefore to be a provider of energy and services to society for an extensive client base alongside a firm commitment to the environment, taking a position of leadership regarding our stakeholders and shareholders, optimizing efficient capital allocation from our existing businesses to renewable energy generation, and placing clients at the center of our strategy, positioning ourselves in the top quartile of the energy industry in shareholder remuneration and maintaining financial strength at a time of high uncertainty.

The crisis unleashed by the COVID-19 pandemic has had a harsh impact on the oil industry. To what extent has this event impacted the definition of Repsol’s new strategic plan? Has the crisis accelerated the Group’s roadmap to a more diversified business?

The appearance of COVID-19 in the world over one year ago has represented the most considerable disruption in many aspects since World War II. For the sector of integrated companies like Repsol, it was the “perfect storm” due to the impact on oil price reductions observed in the first part of the year and the drastic fall in refining margins. The level of contraction of demand has been comparable to the economic reduction seen primarily in the countries where Repsol operates with annual drops greater than 15%. Furthermore, there has been a particularly notable impact on our resource generation capacity in 2020.

Since March 2020, the company has focused its efforts on ensuring financial balance against a backdrop where all the risks materialized. By launching a Resilience Plan, we were able to finish the year even with a reduction of the net debt over the previous year, in an effort focused on optimization, efficiency, and efficient selection of products.

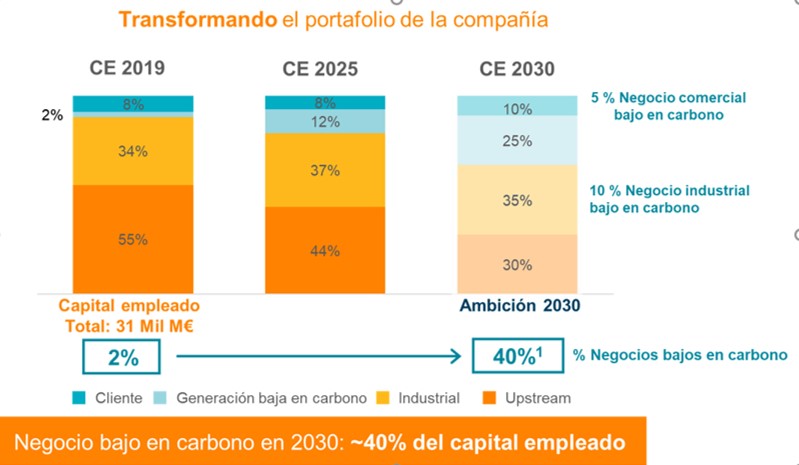

That said and taking into account the current situation of uncertainty in which the strategic plan was presented, Repsol has established two periods in the plan’s timeframe: an initial phase in 2021 and 2022 where our objective is focused on guaranteeing excellent performance in our operations and financial strength in an environment of economic uncertainty and high volatility, leveraging efficiency and capital discipline to maintain the initiatives established for the energy transition; and a second phase from 2023 to 2025 where we aim to accelerate transformation and growth generation by optimizing the portfolios of our existing businesses, creating new, higher-intensity business platforms from our investments, improving our operating and financial ratios with a plan that can be self-sustainable in spite of restrained global energy prices, and delivering greater value for shareholders. This transformation can be seen with greater diversification of the company’s capital used and greater importance placed on low-carbon generation and industrial business, including alternative energy sources like hydrogen and sustainable biofuels.

Among the various renewable energy sources, which will take a leading role in this new stage for Repsol?

Repsol has been committed to low-carbon power generation sources for many years, with more than 3000 MW in operation in 2020 coming from wind, photovoltaic, hydraulic, cogeneration at our industrial complexes, and combined cycle energy, which are fundamental to compensate for the erratic nature of wind and solar energy.

Specifically, for renewable energy, we are already developing six renewable energy projects in Spain. Last year, the first Delta wind turbines in Aragón were connected to the grid, and work was begun on the Valdesolar and Kappa photovoltaic projects. There is also a joint venture in place in Chile with Ibereólica that provides us with access to a project portfolio of more than 1600 MW until 2025 and the possibility of exceeding 2600 MW in 2030. Our commitment for 2025 includes growing to 7.5 GW and 15 GW by 2030 with low-carbon power generation sources—wind and photovoltaic.

In addition to power generation, it is essential to remember that biofuel and hydrogen are also exciting forms of renewable energy that Repsol has included within the framework of this Strategic Plan. Among the 2025 objectives, we expect to produce 1.3 Mt of sustainable biofuels, in addition to 64,000 tonnes/year of renewable hydrogen, reaching an equivalent production of 400 MW.

Lastly, all these products are part of Repsol’s commitment that covers an integrated client vision with high added value services and products to develop and include clients’ new needs (WiBLE car sharing, electric mobility, distributed generation, Waylet app, etc.).

What will this greater commitment to renewable energy look like on an international level? What countries/regions will be prioritized in its implementation?

Our project and asset pipeline is currently limited to the Iberian Peninsula and Chile following the finalization of an agreement with Ibereólica in 2020 to implement new projects in the latter, which offers a highly sophisticated market with a stable, mature regulatory framework. Our ambition is to develop a portfolio and explore opportunities in other markets that can complement our portfolio and where we can have competitive advantages both due to our traditional presence and our differential capacities.

Repsol has been researching and improving energy for transportation for some time. This year, it reached a major milestone—producing the first batch of biofuel for aviation in the Spanish market—at its Puertollano industrial complex. What were the primary challenges the company faced in developing this?

We are proud to be the first to produce sustainable fuel for aviation in Spain. This industry is undoubtedly fundamental to decarbonizing the economy and will again be critical in conversations when the acute situation we are experiencing is over. These 7000 tonnes of bio jet fuel passed the stringent testing established for this product type, and we expect production will be expanded to other Repsol facilities in Spain. Proof of this is that, several days ago, we announced the production of a new batch of 10,000 tonnes from biomass at our Tarragona complex.

The need to ensure the raw material for production stands out from among the challenges presented by this fuel type. That is why Repsol uses a multi-technological approach with a diversity of raw materials that, as can be seen in the plan, range from biomass to urban waste.

In addition to developing biofuels, what other lines of research are being carried out in the Group on the path to achieving the CO2 emission reduction objective?

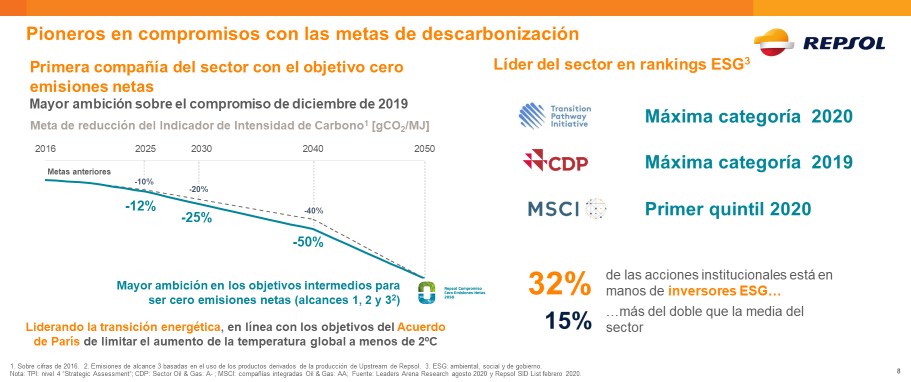

First, I would like to note that, in December 2019, Repsol was the first company that took on the formal commitment to progress to zero net emissions by 2050, to the extent that 40% of the CEO’s long-term incentives are associated with this objective. Second, it is important to note the importance of the emissions reduction measurement mechanism, which takes into account the entire value chain from production/generation to consumption. Lastly, in the latest strategic plan, we increased the emission reduction intermediate objectives from 10 to 12% by 2025, 20 to 25% by 2030, and 40 to 50% by 2040. A final significant consideration is the inclusion of carbon pricing and all of the company’s investment decisions. We want to continue being leaders in the energy transition, while we create value for our shareholders and society.

The objective to reduce carbon intensity covers all Repsol’s businesses. The exploration and production business unit is leading the decrease in carbon intensity with a 75% reduction, placing us on the cutting edge of portfolio management, optimizing production of new barrels with lower carbon intensity, and developing capture and storage projects for some development projects or assets, such as Indonesia.

The industrial business unit is focused on development and adoption of improved technology, searching for opportunities to use energy, optimize tools, and digitalize operations through new projects like an advanced biofuel plant at the Cartagena refinery, several circular economy projects in the chemical business for both used plastic recycling and mechanical polyolefin recycling, a biogas power generation plant using municipal waste, and zero net emission synthetic fuel plants. It is also notable that Repsol has the largest green hydrogen project at Petronor, keeping in mind that Repsol is the top producer and consumer of hydrogen in Spain.

In the client business, we are expanding sales of low-carbon electricity, in addition to developing energy solutions based on our platform of over one million natural gas and electricity clients and dual platforms for advanced mobility, without setting aside the technological development of new fuels and engines that ensure a substantial improvement in emission reduction.

Lastly, our commitment also means that, for the part that we cannot cover with current technological developments, we can offer nature-based solutions with cooperation agreements for reforestation, such as the joint venture comprising Fundación Repsol, Sylvestric, and Land Life.

One of the projects that you have announced along these lines is constructing a plant to produce zero net emission fuels from CO2 and green hydrogen, generated with renewable energy. What type of applications does green hydrogen have specifically? What is its outlook for the future?

I would like to answer this question first by analyzing the applications of hydrogen, Spain’s position as a producing country, and, lastly, Repsol’s strategy.

There are multiple applications for hydrogen, ranging from direct use in industry as raw material and for heat generation, synthetic fuel production, direct mobility, injection into current natural gas networks, or as renewable energy storage for later use.

Spain has exceptional conditions to develop renewable hydrogen production because of its installed capacity, renewable energy potential—biomass, solar, and wind—its geography and proximity to markets, and efficiency in associated production costs. It is important not to forget that renewable hydrogen can be made from water electrolysis and biomethane reforming.

Repsol is the largest consumer and producer of hydrogen in Spain, with 72% of the market share. This prime position enables Repsol to conciliate between self-supply and other uses, taking advantage of the service station network for transportation and synthetic fuels and supplying the natural gas network with a mixture for use in industrial-domestic heating, as a raw material for other industries, and as energy storage to increase flexibility in renewable electricity generation.

Repsol also can produce renewable hydrogen from biomethane at its own facilities, which will allow us to offer competitive prices in the short term, in contrast with the other producers.

Renewable hydrogen will play an important role in the energy and industrial context of our country and the European Union, as it is a fundamental part of the solution to achieve emission neutrality. Spain has set the goal of having 4 GW of capacity in 2030. Repsol will contribute with a capacity of at least 1.2 GW by that year.

The restructuring of Repsol’s business has also been observed in the electricity sector, where the Group has exponentially increased its capacity. What are the objectives driving it in this new stage?

As I said before, our objectives for 2025 is to reach a base of 7.5 GW of low-carbon generation and double it to 15 by 2030, where international presence must take on about 50% of total operational capacity. In addition, focusing on clients, our objectives include expanding the current base of natural gas and electricity clients from one million clients to 2.5 in 2025. This client base is understood as comprising the unique offer of digital clients, multi-product clients from natural gas, electricity, butane, propane, fuel at our service stations or other lubricant and specialty channels, and various product-associated services. Let’s not forget that we have over 10 million registered clients for a base of 24 million active clients in Spain.

In addition, as I said above, we want to support our clients on their path to emission reduction, progressively providing them with more products and services that enable them to reduce their carbon footprint.

Regarding the Group’s upstream and downstream activities, what is the growth outlook for the coming years?

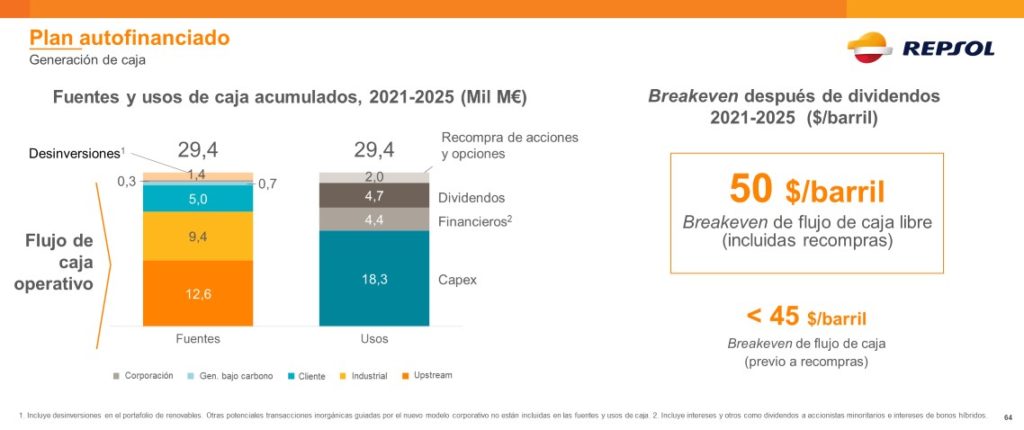

Our upstream priorities in the strategic plan for the 2021-2025 period include prioritizing free cash flow with efficiency in costs and the asset portfolio, assuming a Brent price of $50 per barrel as a working base for this period.

Business management will also focus on prioritizing projects that generate value in the short and medium-term and leveraging digitalization and cost-efficiency. From the standpoint of production targets, it is worth noting our preference for value over volume, committing to around 650,000 barrels of oil equivalent a day during the plan’s five years in effect, thereby reducing the number of countries where we are present and concentrating our exploratory activity to four or five relevant areas. These objectives will be perfectly compatible with a reduction in carbon emission intensity of 75%, and we will sell any non-strategic or excessively carbon-intense projects.

Regarding the industrial business, having already mentioned the client and renewable energy generation businesses, the focus in refining will be on improving competitiveness by maximizing margins, optimizing costs, and increasing the business associated with new decarbonization platforms where we have, or create, a component in the differential margins compared to our competitors. Our position in Europe in the top quartile should help us in this regard.

In the chemical business, the strategy includes differentiation through products with a higher added value, selectively growing with new opportunities, and creating and developing circular economy platforms (recycling and chemical products from waste). Trading will continue increasing its contribution to the company by integrating value from the assets and growth in key markets and products.

Lastly, it is important to note that this business will be fundamental in Repsol’s transformational vision, combining our current assets with the decarbonization and circular economy projects that make a substantial change to the assets throughout the plan to provide improved products in the future.

From the large-scale company perspective, what would be the greatest contribution from this transformation of the business?

Based on a profound commitment to the surroundings in the countries where we operate and the environment globally, we have led the commitment to zero emissions by 2050 throughout the industry. We also understand that this global objective is a differential strength in the company’s transformation, the foundations of our team, our existing assets, and their necessary adaptation and transformation to continue developing the industry and the services to an extensive client base. To that end, we have an investment program of over €18 billion over the next five years, of which close to a third will be allocated to low-carbon initiatives, considering our financial needs and maintaining a differential value offer for our shareholders with almost €5 billion of dividends over the next five years. Depending on the environment, we can launch share buyback programs that increase our shareholders’ participation in the company.

From the standpoint of risk management, what impacts can be expected? How do you believe this strategic plan can affect your risk and, ultimately, your insurance program in the future?

While it is true that new activities entail new risks, we believe that the risks that can arise from the energy transition are similar—and with less exposure in most cases—to the risks the company manages typically. They would be included in the company’s integrated risk system naturally without significant obstacles.

For several years, the insurance program has already considered including assets associated with low-emission businesses (cogeneration, hydroelectric, renewable energy). We, therefore, do not anticipate any issues to integrate them properly. However, we do envisage continuous monitoring and possible slight adjustments in the program to provide the best solution.

MAPFRE is the top insurance company of the Repsol Group, and their connection goes back more than 30 years. If you had to describe the foundation of this relationship briefly, what would you highlight and why?

First, I would like to list the relationships that the MAPFRE and Repsol groups have enjoyed for many years. MAPFRE is the Repsol group’s top insurance company for industrial risks by capacity. MAPFRE is the company that enables us to implement an international insurance program in almost 30 countries, and it is, therefore, our insurer in those countries. MAPFRE is also the company to which we transfer part of the risks retained on a corporate level. Lastly, MAPFRE actively participates in construction projects in our risk engineering program and is our most trusted insurance company in direct policies for significant specialty risks.

Any long-term relationship is based on a multitude of factors. To list some parts of the foundation of a successful understanding, in the specific case of MAPFRE, we could note the continual improvement that comes back as a mutual benefit, trust, and transparency, in addition to the capacity to maintain a balanced relationship and provide support when difficulties arise regarding each side’s activity.

And lastly, considering the path taken in the energy transition, do you believe that a world based 100% on renewable energy is viable in the medium/long-term?

It is important to differentiate the ends from the means to ensure an adequate analysis. The shared objective worldwide is to move toward progressive decarbonization inclusively. To that end, it is vital to create sufficient incentive so that all the technologies can compete on equal footing in working towards achieving the objective. Otherwise, we will be deterministic, confusing the ends with the means and inhibiting the capacity of technological improvement associated with this inevitable energy transition. In this scenario, we are heading for a world where greater importance is placed on renewable energy, where there will continue to be transitional energy sources like natural gas, and where other energy sources like oil will play a fundamental role in certain applications and products that are difficult to replace in the short and medium-term, as well as a technological improvement that also helps in the overall objective. Repsol will be part of the solution and wants to lead that transition based on its current assets, its profound transformation toward decarbonization and the circular economy, the expansion of its renewable power generation base, and its ability to provide high-quality products services to a larger, more demanding client base.