06/05/2022

The European gas industry is looking eastward, keeping a watchful eye on the impact of the war in Ukraine on the security of energy supplies and costs. In this context, and since the conflict began, the Spanish Gas Association has been working with national and international administrations to identify risks and develop short-, medium- and long-term solutions. Its Chairman, Joan Batalla, tells us about the role that Spain can play in this delicate geopolitical situation.

How does the Ukraine war affect – or how may it affect – the European gas industry. And what impact is it having on Spain?

The conflict in Ukraine has led to great volatility in prices for energy raw materials and has brought to the fore the relevance of supply security and the importance of diversification of supply sources, as well as the promotion of clean energy alternatives, in line with the European Union’s decarbonization targets. The recent European Parliament resolution requesting a total embargo on energy imports from Russia must also be taken into account.

In its REPower EU plan (to reduce its dependence on Russian gas), the European Commission mentions boosting biomethane production as one of the key measures to attain new energy sources. It is committed to doubling the target proposed in the Fit For 55 legislative package to reach production of 35 billion cubic meters per year by 2030. The Spanish gas system is already prepared to transport renewable gases such as biomethane (and in the future, green hydrogen).

It is essential to continue working to roll out Spain’s full potential so as not to miss the opportunity presented by the high degree of technological maturity already achieved throughout the renewable gases value chain and the resources and capabilities that our country has. It is crucial to analyze the development of the appropriate support mechanisms in greater detail, from the standpoint of supporting biogas-biomethane production and its injection into gas networks.

What is the demand for gas in Spain? Who are its main consumers?

In 2021, natural gas demand in Spain increased by 5% compared to the previous year, at about 378.4 TWh. This figure is 9.2% higher than the average of the last ten years and the second highest since 2011. Growth is largely due to the recovery of economic activity following the impact caused by the Covid-19 pandemic in 2020 and the colder temperatures recorded at the beginning of the year.

By sector, the conventional demand for households, businesses and industry increased by 6.2% to 288 TWh, while demand for electricity generation increased by 1.6% to reach 90 TWh, a number which ranks as the second highest demand since 2011. In this regard, it is important to highlight the role of combined cycles, which prevented the collapse of the electricity grid during an unprecedented snowy, cold spell, guaranteeing the supply of electricity to homes and industries thanks to its flexibility and efficiency.

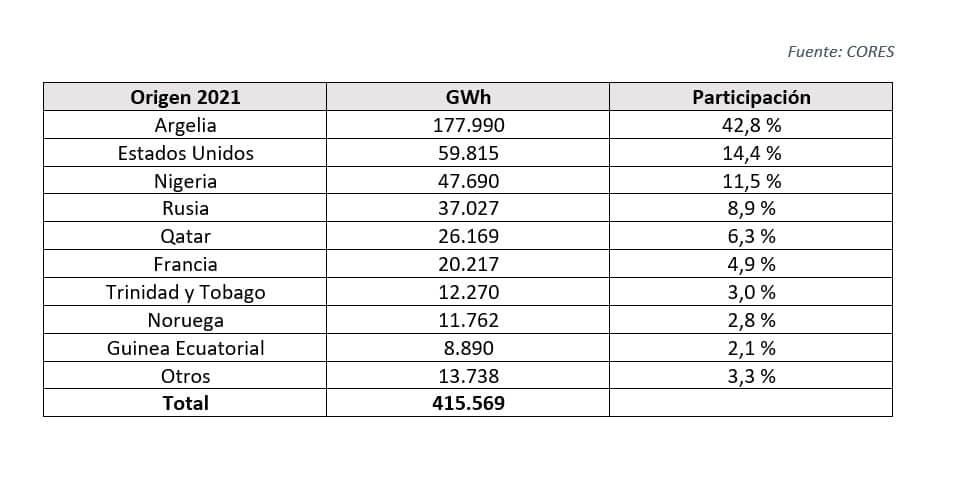

Where does the gas used in Spain come from?

For decades, the Spanish gas system infrastructure network has been a European benchmark due to the diversification of its supply.

The system has international pipeline connections with Portugal, France and Algeria. We also have the infrastructure to receive, store and regasify liquefied natural gas (LNG), which is the highest capacity in Europe, key to ensuring the security of supply in our country.

There are six plants spread across the entire Spanish coast, where LNG undergoes a regasification process, in which gas that arrives by ship in a liquid state is converted into a gaseous state. This is necessary to be able to inject it into the gas transport and distribution networks and transport it to the points of consumption: households, industries and electric power plants (combined cycles). LNG supply accounted for 54% of Spain’s total gas supply in 2021 and the total distribution from different sources was as follows:

What are Spain’s storage and regasification capacities?

Spain has a total LNG storage capacity of 3,316,500 cubic meters, spread over the 25 tanks available to the six receiving plants we have: Barcelona, Huelva, Cartagena, Bilbao, Sagunto and Mugardos. The maximum vaporization (regasification) capacity of these plants is 6,862,800 Nm3/h.

Spain has the largest LNG storage and regasification capacity in the EU and the UK; one-third and just over one-quarter, respectively. This potential allows Spain to deal with the current crisis triggered by the Russian invasion of Ukraine with greater calm than its neighbors, at least in terms of supply security.

Do we have a regulatory context that favors the industry as a lever in the decarbonization of energy?

Renewable gases, particularly biomethane, contribute to the reduction of CO2 emissions and promote the circular economy, solving a waste management problem. In this sense, with the necessary public-private partnership, we estimate that with biomethane, practically 50% of the current demand for natural gas for industrial and household-commercial use (conventional demand) in Spain could be decarbonized, so it is necessary to set ambitious short-term goals.

On March 30, Royal Decree-Law 6/2022 was published in the Official State Gazette, by which urgent measures were adopted within the framework of the National Plan to respond to the economic and social consequences of the war in Ukraine. This included a number of specific provisions relating to renewable gases, but – as with the Biogas Roadmap – it represents yet another missed opportunity to boost and develop renewable gases.

In the current context of committment to the diversification of the sources of origin and the security of supply using renewable gases, the proposals included do not align with Spain’s potential or with the European Commission’s 2030 targets.

How do they impact Spain’s potential and international challenges?

The measures proposed to expedite the processing of renewable electrical energy projects are completely asymmetric compared to renewable thermal energy projects. They limit treatment to the injection of biomethane into gas networks and do not grant them the status of public utility facilities. So they are excluding them from the expropriation and consultation processes included in the Hydrocarbons Law.

These provisions go against the alleged objective of favoring the rapid deployment of renewable gases, which would contribute to reducing dependence on foreign energy sources. Morever, this jeopardizes the feasibility of a significant number of projects, as it delays their implementation and gives rise to unnecessary legal insecurity.

It is time to move forward with the deployment and adaptation of infrastructure to use all renewable gases. On one hand, by being more ambitious with the objectives that our country can take on as a biogas and biomethane producer. An on the other hand, by continuing to expand interconnections with Europe.

Could Spain become Europe’s hub? Where do you start from and what challenges do you face?

In the current context, Spain can play a critical role as a hub to supply gas to our European partners, leveraging its infrastructure and storage and regasification capacity.

An infrastructure which, on the other hand, must keep improving, especially in the area of expanding interconnection capacity with France, in line with REPower EU. These investments must be understood above all as being medium- and long-term solutions. At this point, it should be remembered that through these infrastructures, renewable gases such as biomethane or green hydrogen can circulate in a cost-effective way. These gases will be essential in Europe’s green future and energy transformation.

How can Spain’s geographically strategic position be taken advantage of?

If we had suitable and sufficient capacity to export through the Pyrenees, Spain could improve the security of gas supply in Europe. The nominal (reversible) capacity for export to France (Europe) is 225.00 GWh/d. Therefore, the possibilities of sending gas to the countries most at risk of potential disruption to supply from Russia is limited (despite having the relevant infrastructure to receive LNG and the gas pipeline that transports gas from Algeria).

With the MidCat project – the incomplete Spain-France gas pipeline through Catalonia – export capacity to Europe would have doubled. That potential transfer of gas (originating from North Africa or regasification plants) would not eliminate Europe’s heavy dependence on Russia, but it would change the current numbers.

It would be a step forward towards establishing a greater balance and would be of significant strategic importance, even more so with the start-up of other new regasification plants in Europe (such as those that Germany seems to want to develop immediately).

As a result of the conflict in Ukraine and the EU’s decision to reduce its energy dependence on Russia, energy interconnection projects between Member States take on a new perspective.

Security of supply is the priority today. But interconnection infrastructures are also a key tool to reach domestic market targets. Due to its geographical position, the Iberian Peninsula is one region that has a limited degree of interconnection with the rest of the European market. Therefore greater efforts are required for the integration of the electricity and gas markets in Europe.

This infrastructure would not only make it possible to meet current needs in the medium term (it would take 2–3 years to develop), but also over a longer time horizon, beyond 2030, like a pipeline to transport renewable or low-carbon gases produced in Spain or even in North Africa. A response in line with the European gas industry’s commitment to decarbonization and aligned with the European Union’s climate and supply security targets.

Joan Batalla is the President of the Spanish Gas Association, SEDIGAS. Batalla has extensive professional experience in the energy industry. Since 2015, he has held the position of Managing Director of the Foundation for Energy and Environmental Sustainability (FUNSEAM), a non-profit institution whose mission is research in the field of energy economy and the promotion of energy and environmental sustainability.

Joan Batalla is the President of the Spanish Gas Association, SEDIGAS. Batalla has extensive professional experience in the energy industry. Since 2015, he has held the position of Managing Director of the Foundation for Energy and Environmental Sustainability (FUNSEAM), a non-profit institution whose mission is research in the field of energy economy and the promotion of energy and environmental sustainability.

Between 2005 and 2011 he was the Director of the Chairman’s Office at the National Energy Commission (CNE) which is currently part of the National Commission for Markets and Competition (CNMC). He subsequently held the position of director of this organization and was responsible for defining the implementation of the energy industry’s regulatory framework in Spain until 2013.

He received a Bachelor of Science in Economics from the University of Barcelona and a Doctor of Economics – Extraordinary Doctorate Award from the Rovira i Virgili University. He completed his training with the General Management Program of the University of Navarra Business School and a Master’s in Energy Regulation from the Florence School of Regulation of the European University Institute. In 2011, his research and academic work was recognized when he was awarded the “Joan Sardà Dexeus” Economics Prize for the paper “Catalan Industry after the Crisis.”